If you’re staring at a wet ceiling, warped floors, or a soggy pile of towels, you’re really asking one thing: does homeowners insurance cover water damage in your situation. The frustrating part is that water is both common and complicated in a homeowners insurance policy. Coverage usually hinges on how the water got in, how fast it happened, and whether it looks like something that could’ve been prevented with normal upkeep. In this guide, you’ll get a clear way to think about “covered vs. not covered,” plus a practical playbook for what to do right after you spot water damage so you don’t accidentally make a claim harder than it needs to be.

Best for: Homeowners dealing with a new leak or overflow who need fast clarity on coverage, documentation, and next steps.

Not ideal when: The damage built up for weeks or comes from groundwater, foundation seepage, or a known maintenance issue you delayed fixing.

Good first step if: You can safely stop the water, take photos, and limit spreading damage before deciding whether a claim makes sense.

Call a pro if: Water is near electrical, sewage is involved, ceilings are sagging, or you can’t identify and stop the source quickly.

Quick Summary

- Coverage usually comes down to whether the cause was sudden and accidental, not gradual damage or neglect.

- Many policies cover the resulting damage, but not the repair that fixes the broken part that caused the leak.

- Flooding and groundwater intrusion are typically separate from standard homeowners coverage.

- Sewer/drain backup and sump pump overflow often require a specific endorsement.

- Fast mitigation and clean documentation can make the adjuster process far smoother.

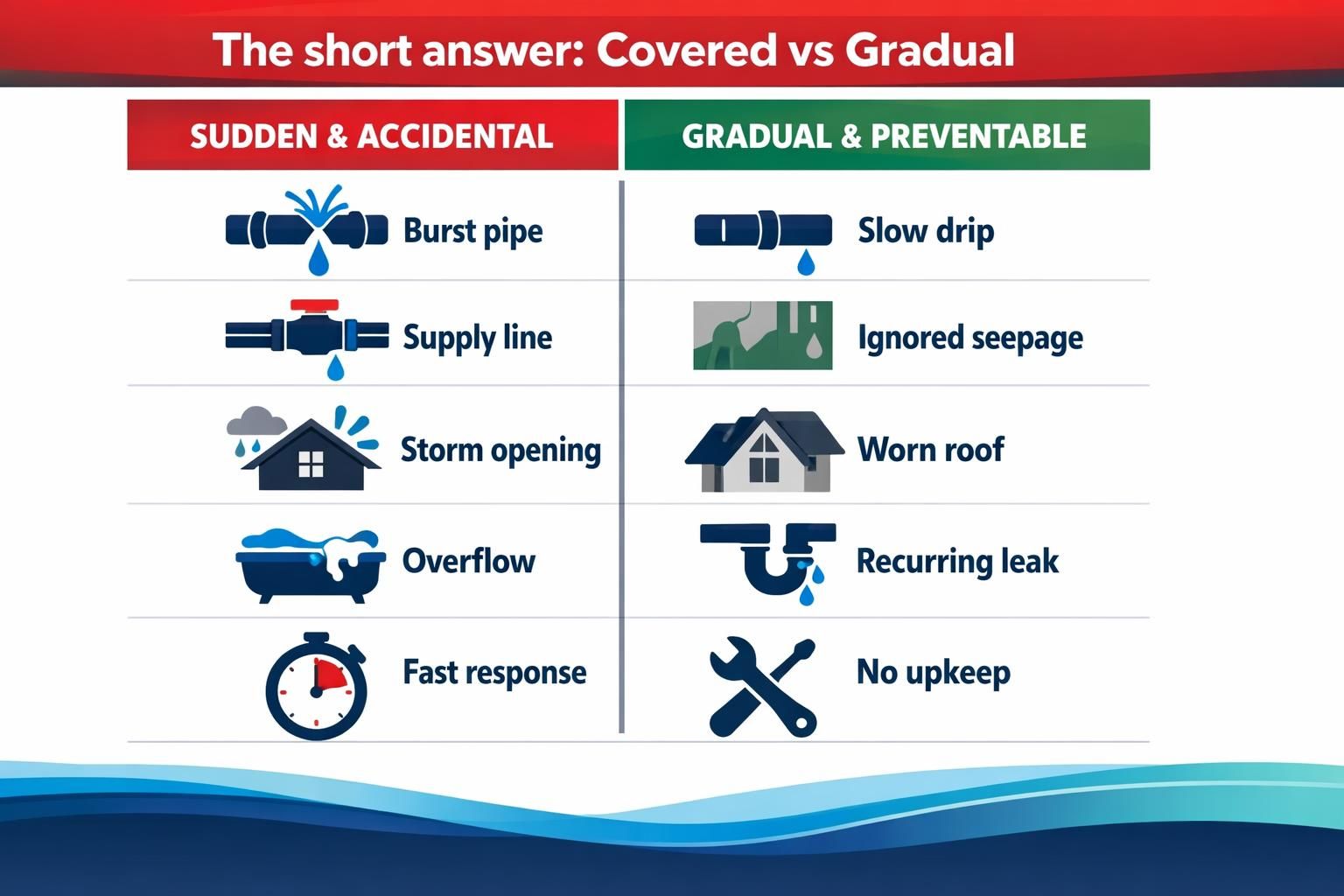

The Short Answer: “Sudden and Accidental” Vs. “Gradual and Preventable”

Water damage is most likely covered when it’s sudden and accidental, and least likely covered when it’s gradual and preventable. Insurers care as much about why it happened as how bad it is, because exclusions often target wear, neglect, and maintenance issues.

Sudden and accidental examples include a burst pipe, a one-time supply-line failure, or rain entering through a storm-created opening. The water appears quickly, wasn’t reasonably predictable, and you act to stop it and mitigate.

Gradual and preventable examples include a slow sink drip that rots cabinets, recurring toilet seepage you ignore, or a long-term roof leak that stains the same area repeatedly. Even with a covered cause, failure to shut off water or dry promptly can create denial risk for poor mitigation.

Water Damage Homeowners Insurance Typically Covers

Most policies cover water damage from a sudden, accidental release inside the home or from a covered peril that lets water in. If something breaks unexpectedly and damages drywall, floors, cabinets, or belongings, that’s the scenario the policy is designed for.

Coverage usually targets resulting damage: extraction, drying, removal of damaged materials, and repairs. Early priorities are stopping the flow, limiting spread, and documenting before cleanup. For a fast triage list, see stop damage from spreading.

Also, water used to extinguish a fire can be covered as firefighting water damage tied to a covered peril.

Common Covered Scenarios (Burst Pipe, Appliance Leak, Storm-created Opening)

Burst pipes are classic covered losses because they’re abrupt. Appliance leaks can qualify when they’re clearly a one-time failure, like a dishwasher hose or refrigerator line crack. Storm intrusion may be covered when wind or debris creates a new opening and rain enters, not when it seeps through a long-term weak spot.

Water Damage Homeowners Insurance Typically Won’t Cover

Homeowners insurance typically won’t cover water damage tied to flood, groundwater intrusion, foundation seepage, or slow leaks linked to wear and tear, neglect, or delayed maintenance. Policies focus on sudden events, not ongoing conditions.

Flood is the big exclusion. If water rises from outside and enters the home, it’s usually a flood even if it’s shallow or fast, and you’re pushed toward flood insurance.

Groundwater seepage through foundation walls is also commonly excluded based on the entry pathway.

Slow leaks often trigger denials. Staining, rot, corrosion, or long-standing mold can signal gradual damage or a known problem you didn’t fix, which insurers may label “neglect.”

In multi-unit situations, responsibility can involve you, the building, and neighbors. For the tenant angle and coordination steps, see apartment water damage steps.

Flooding, Seepage/groundwater, and Long-term Leaks

Flooding is usually excluded unless you have separate flood insurance, and groundwater intrusion or foundation seepage is often excluded even when there’s no obvious “flood.” Long-term leaks are also a frequent no, especially when there are signs the issue wasn’t new. If the water path or damage pattern screams “this has been happening,” the insurer may treat it as preventable gradual damage rather than a covered water damage claim.

Special Cases People Ask About

Roof leaks, mold, frozen pipes, and toilet overflows are classic “it depends” claims. The decision often turns on the trigger event versus the condition that allowed it.

Roof leaks are more likely covered when a storm creates a new opening and rain enters. Leaks tied to worn shingles, old flashing, or repeated seepage usually look like maintenance and gradual damage, even if the ceiling looks the same.

Mold can be covered when it directly follows a covered water event and you acted quickly to dry. Mold tied to long-term humidity, an ignored leak, or recurring intrusion is commonly excluded or capped.

Frozen pipes may be covered if you used reasonable care: maintained heat, didn’t leave the home unprotected, and addressed obvious freeze risks.

Toilet overflow can be covered when it’s sudden, accidental, and limited (often clean supply water). Repeated clogs, poor maintenance, or sewage backup typically require special coverage. For fast containment steps, what to do fast is useful.

Roof Leaks, Mold, and Frozen Pipes

Roof leaks are more likely covered when a covered peril creates the opening, and less likely when aging materials or deferred upkeep caused the leak. Mold is strongest when it follows a covered loss and you dried quickly; long-term moisture mold is often excluded. Frozen pipes may be covered if heat was maintained and reasonable precautions were taken.

Sewer/drain Backup and Sump Pump Overflow (and the Endorsement You Need)

Sewer backup, drain backup, sump pump overflow, and sump pump failure often require a water backup endorsement because many standard policies exclude them. The damage looks similar to a burst pipe, but insurers classify it based on where the water came from.

If wastewater backs up through a toilet, floor drain, or sink, it’s usually “sewer/drain backup,” not a supply-line leak. If a sump pump can’t keep up or fails during heavy rain, the resulting water is commonly treated as sump overflow or failure, again pointing to an endorsement.

Check your declarations page for terms like water backup endorsement, sump overflow coverage, or similar add-ons. If you have it, document the backup point clearly because that’s the trigger. If you don’t, get an estimate anyway, but expect out-of-pocket costs.

Basements get messy fast when backup versus seepage isn’t clear. For an action plan, use basement flood next steps.

What Your Policy Pays for (and What it Usually Won’t)

Most policies pay for resulting damage, not the part that failed. This “source-of-loss vs. resulting damage” split drives many disputes.

Often covered: water extraction, drying/dehumidification, removal of damaged drywall or flooring, and rebuilding. Some policies also cover cleaning and limited contents restoration. If walls or floors must be opened to reach wet areas, “tear-out/access” may apply, depending on wording.

Often not covered: repairing or replacing the broken item itself, such as a worn hose, failed pipe section, old water heater, or roof materials that simply aged out. Hot water heater failures are a common example: the policy may cover the water damage from a sudden leak, but not the new water heater if it failed due to wear and tear.

Factor in your deductible and claim history. For small losses, paying out of pocket can be reasonable; for larger, hidden damage, filing may be safer.

Dwelling Vs. Personal Property, Tear-out/access, Source-of-leak Repairs

Dwelling coverage applies to structure items like drywall, flooring, cabinets, and framing. Personal property covers belongings like furniture, clothing, and electronics. Tear-out/access may pay to open walls or floors to reach damaged plumbing, but usually not to upgrade systems. Source-of-leak repairs are often yours, even when resulting damage is covered.

How to File a Water-damage Claim (Step-by-step)

Water-damage claims go smoother when you stop the loss, document everything, and keep the facts consistent from the first call through the adjuster visit. Move fast, but don’t skip proof.

Practical sequence:

- Make it safe: shut off the water. If water is near outlets or panels, consider cutting power. If unsure, see when to shut off power.

- Stop and contain: catch drips, move valuables, block spread with towels or plastic.

- Document before demolition: photos and video of the source, the water path, and each damaged room (wide shots and close-ups).

- Start mitigation: drying, dehumidification, and removing saturated items if safe. For pro help, emergency water extraction help.

- Call your insurer: report the claim, log names, dates, and instructions.

- Save receipts: rentals, emergency repairs, and temporary housing if needed.

- Meet the adjuster: walk through cause, timing, and damage with your evidence.

- Keep failed parts: hoses, fittings, or valves help prove “sudden and accidental.”.

How to Reduce the Chance of Denial and Prevent Future Damage

Denial risk drops when you act quickly, document clearly, and avoid anything that looks like long-term neglect. Your goal is to make the cause and timeline easy to understand and consistent with “sudden and accidental.”

Do these:

- Write a timeline: discovery time, shutoff time, who you called, when drying began.

- Photograph hidden areas as you open them: insulation, subfloor, backs of drywall, and wet framing.

- Start drying immediately: standing moisture invites mold and complicates coverage. Use drying a room fast as a first-day checklist.

- Fix the source: even if the policy won’t pay for the failed part, recurring water kills the claim.

- Maintain the home: replace aging supply lines, address corrosion, and repair small roof issues early.

- Review endorsements: sump pump and backup coverage should match your property’s risk.

Before filing, compare deductible versus likely scope, including moisture you can’t see behind walls or under floors.

Conclusion

Most of the time, the answer to does homeowners insurance cover water damage is “yes, if it’s sudden and accidental and you act quickly,” and “no, if it’s gradual, preventable, or excluded like flood or groundwater intrusion.” Your best next step is simple: stop the water safely, document the cause and the damage clearly, and start mitigation so the loss doesn’t expand. Then compare the likely covered repairs to your deductible and decide whether filing a water damage claim makes sense. If anything involves sewage, electrical risk, or widespread saturation, treat it like an emergency and get qualified help fast.